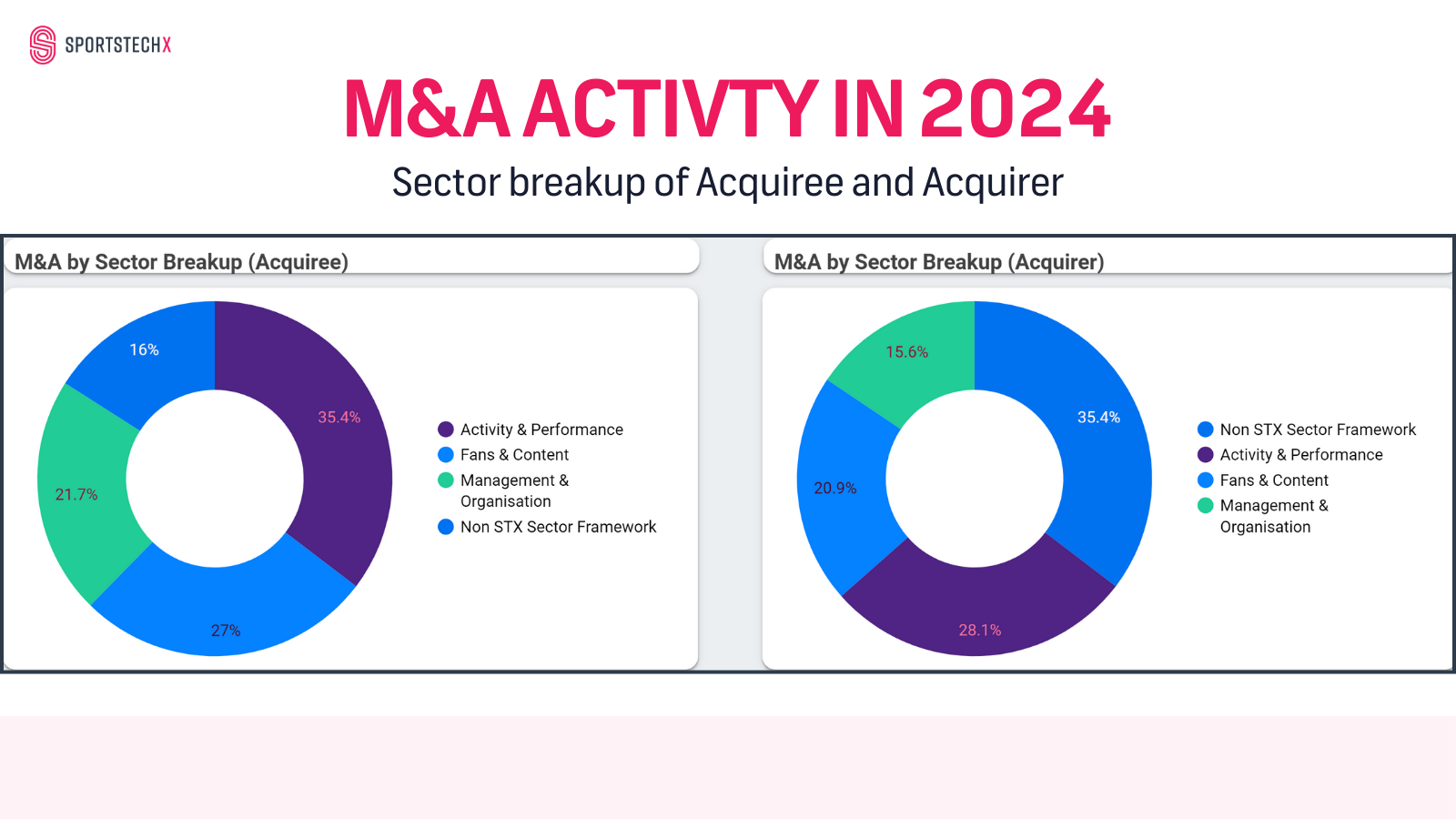

The sports tech M&A market in the last 5 years experienced fluctuations in both deal volume and transaction value. We called 2023 ‘The year of consolidation’, 2024 has seen more but nothing like last year. Total M&A deals in for the period 2020-2024 amounted to $26.3 billion across 263 transactions. The highest peak occurred in 2023, when the sector saw deals worth $10.9 billion, increasing consolidation across the industry. However, this momentum was tempered in 2024, with a $4.36 billion in disclosed deal values. Among the major transactions in the past year, noteworthy deals included: Snaitech (Italy) was acquired by...